Commoditized Wisdom: Report (Week Ending February 9, 2024)

Posted:

Key points

Energy prices, except for natural gas prices, were higher. Oil prices rose 6%, gasoil and heating oil prices gained 11% and gasoline prices increased 9%. Natural gas prices fell 11%.

Energy prices, except for natural gas prices, were higher. Oil prices rose 6%, gasoil and heating oil prices gained 11% and gasoline prices increased 9%. Natural gas prices fell 11%.- Grain prices again were mainly lower. Kansas City wheat prices fell 4%, Chicago wheat and soybean prices fell about ½ percent and corn prices dropped 3%. Soybean oil prices rose 6%.

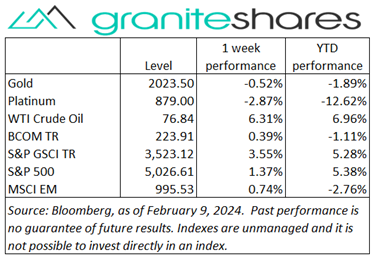

- Spot gold prices decreased 1%, spot silver prices fell about ¼ percent and spot platinum prices dropped 2%. Palladium prices fell 9%.

- Base metal prices were all lower. Zinc and lead prices fell between 5% and 7%, copper prices lost 4% and nickel prices dropped 2%. Aluminum prices were down 1%.

- The Bloomberg Commodity Index rose 0.4%. Gains in the energy and soft sectors were partially offset by losses primarily in the base metals sector but also by losses in the precious metals and grains sectors.

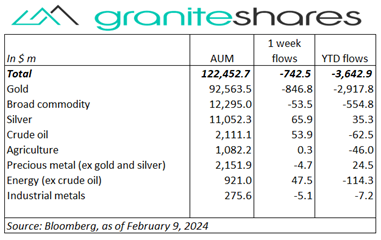

- Larger outflows from gold ETPs partially offset by energy and silver ETP inflows.

Commentary

Major stock indexes moved higher again last week with the Nasdaq Composite Index significantly outperforming the S&P 500 Index and, in particular, the Dow Jones Industrial Average. The week started on a down beat, with stock markets reacting to hawkish Powell comments Sunday and stronger-than-expected service sector growth. Stock indexes, however, moved higher the remainder of the week, predominantly propelled by strong tech stock performance despite markedly higher long-term Treasury rates. While rate cut expectations declined and Treasury rates rose, tech stocks (in particular Nvidia) rose to new highs, bolstered by growing “soft-landing” expectations. The S&P 500 Index closed above 5,000 for the first time. For the week, the S&P 500 Index rose 1.4% to 5,026.61, the Nasdaq Composite Index gained 2.3% to 15,990.66, the Dow Jones Industrial Average was almost unchanged at 38,671.30, the 10-year U.S. Treasury rate rose 16bp to 4.08% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) strengthened 0.2%.

Major stock indexes moved higher again last week with the Nasdaq Composite Index significantly outperforming the S&P 500 Index and, in particular, the Dow Jones Industrial Average. The week started on a down beat, with stock markets reacting to hawkish Powell comments Sunday and stronger-than-expected service sector growth. Stock indexes, however, moved higher the remainder of the week, predominantly propelled by strong tech stock performance despite markedly higher long-term Treasury rates. While rate cut expectations declined and Treasury rates rose, tech stocks (in particular Nvidia) rose to new highs, bolstered by growing “soft-landing” expectations. The S&P 500 Index closed above 5,000 for the first time. For the week, the S&P 500 Index rose 1.4% to 5,026.61, the Nasdaq Composite Index gained 2.3% to 15,990.66, the Dow Jones Industrial Average was almost unchanged at 38,671.30, the 10-year U.S. Treasury rate rose 16bp to 4.08% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) strengthened 0.2%.

Oil prices moved sharply higher last week, bolstered by Mideast and Ukraine/Russia tensions and falling fuel stocks. U.S. reprisal strikes in Mideast, Houthi Red Sea shipping attacks, Ukraine drone attacks on Russian refineries and lowered Israel/Hamas ceasefire expectations combined to jolt oil prices higher. Adding to upward price pressures was a much greater-than-expected fall in fuel inventories and the EIA substantively lowering its 2024 oil production forecast. Natural gas prices moved sharply lower in reaction to the Biden’s administration moratorium on new LNG production/facilities.

Spot gold prices moved slightly lower last week, pressured by Fed Chair Powell’s hawkish comments Sunday and higher 10-year Treasury rates. Hawkish comments from other Fed officials Wednesday also weighed on prices as did stronger-than-expected service sector growth. Silver prices were also slightly lower, reacting to the same factors as gold. Platinum prices fell slightly more than gold prices, moving more in line with base metal prices.

Base metal prices moved lower as well last week, reacting to diminished rate-cut expectations (following Powell’s hawkish comments Sunday). Prices moved lower despite China’s pledge to support its stock market, perhaps due to lessened activity in front of next week’s Lunar New Year holiday.

Corn prices moved lower on weak exports, a slightly bearish WASDE report Friday and good Brazil planting progress. Soybean prices, marginally lower on the week, benefited from good export inspection but hurt by favorable South American weather forecasts and a WASDE report only slightly lowering Brazil production estimates. Wheat prices finished lower, affected by favorable moisture conditions in winter wheat growing areas and continued cheap Russian prices.

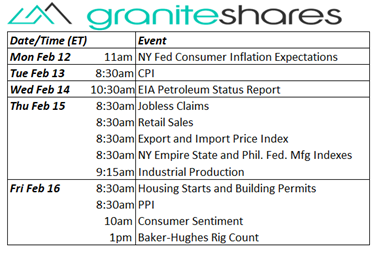

Coming Up This Week

Attention centered on Tuesday’s CPI. PPI Thursday and busy Thursday with jobless claims, retail sales and NY State and Phil. Fed Mfg Indexes.

Attention centered on Tuesday’s CPI. PPI Thursday and busy Thursday with jobless claims, retail sales and NY State and Phil. Fed Mfg Indexes.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.