Commoditized Wisdom: Report (Week Ending February 23, 2024)

Posted:

Key points

Energy prices were mainly lower. Oil, gasoline, gasoil and heating oil prices fell between 2% and 4%. Natural gas prices rose 2%.

Energy prices were mainly lower. Oil, gasoline, gasoil and heating oil prices fell between 2% and 4%. Natural gas prices rose 2%.- Grain prices again were mixed. Wheat prices rose 1% to 2%. Corn and soybean prices fell 3% and 4%, respectively.

- Spot gold prices rose 1% while spot silver and platinum prices fell 2% and 1%, respectively. Palladium prices gained 3%.

- Base metal prices, except for aluminum prices, were all higher. Copper, zinc and lead prices rose 1% while nickel prices rose 7%. Aluminum prices fell 2%.

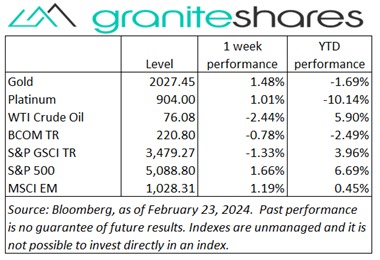

- The Bloomberg Commodity Index fell 0.8 %. Losses in the energy and grains sectors were partially offset by gains in the base and precious metals sectors.

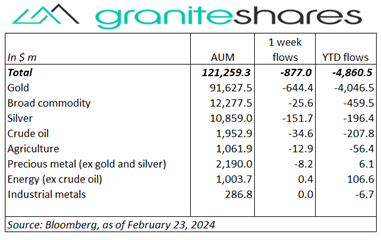

- Outflows from each ETP category with gold ETP outflows accounting for the lion's share.

Commentary

Nvidia’s long-anticipated earnings report drove and directed markets last week. Prior to the report release after hours on Wednesday, stock markets moved lower, affected by an overhang of uncertainty. Markets also were influenced by Wednesday’s FOMC minutes release which revealed “too-early-to-cut-rates” sentiment, adding to downward price pressure. Losses through the close Wednesday, however, were erased Thursday with Nvidia shares rising over 16% on a much better-than-expected earnings report. The gain in Nvidia’s share price helped move all 3 major indexes into positive territory for the week with the S&P 500 Index slightly outperforming the Dow Jones Industrial Average and the Nasdaq Composite Index. Despite the hawkish FOMC minutes, 10-year Treasury rates moved slightly lower and the U.S. dollar actually weakened. For the week, the S&P 500 Index gained 1.7% to 5,088.80, the Nasdaq Composite Index rose 1.4% to 15,996.82, the Dow Jones Industrial Average increased 1.3% to 39,131.53, the 10-year U.S. Treasury rate fell 4bp to 4.25% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) weakened 0.3%.

Nvidia’s long-anticipated earnings report drove and directed markets last week. Prior to the report release after hours on Wednesday, stock markets moved lower, affected by an overhang of uncertainty. Markets also were influenced by Wednesday’s FOMC minutes release which revealed “too-early-to-cut-rates” sentiment, adding to downward price pressure. Losses through the close Wednesday, however, were erased Thursday with Nvidia shares rising over 16% on a much better-than-expected earnings report. The gain in Nvidia’s share price helped move all 3 major indexes into positive territory for the week with the S&P 500 Index slightly outperforming the Dow Jones Industrial Average and the Nasdaq Composite Index. Despite the hawkish FOMC minutes, 10-year Treasury rates moved slightly lower and the U.S. dollar actually weakened. For the week, the S&P 500 Index gained 1.7% to 5,088.80, the Nasdaq Composite Index rose 1.4% to 15,996.82, the Dow Jones Industrial Average increased 1.3% to 39,131.53, the 10-year U.S. Treasury rate fell 4bp to 4.25% and the U.S. dollar (as measured by the ICE U.S. Dollar index – DXY) weakened 0.3%.

Oil prices ended the week lower despite increased Red Sea/Houthi tensions. Interestingly, prices fell Tuesday despite China’s large reduction in its benchmark mortgage rate. Prices moved higher Wednesday and Thursday, bolstered by Mideast/Red Sea tensions but fell markedly on Friday following hawkish Fed officials’ comments. Hawkish FOMC minutes, indicating the Fed was in no rush to lower rates, added to downward price pressure.

Spot gold prices moved higher last week despite hawkish FOMC minutes and Fed officials’ comments. Haven buying, predicated on Mideast tensions, helped buoy gold prices but so did a weaker U.S. dollar and lower 10-year Treasury rates. The U.S. dollar weakened despite reduced expectations of “sooner-than-later” rate cuts, perhaps on profit taking. Spot silver and platinum prices moved lower, giving up some of last week’s noticeable gains.

Base metal prices mainly moved higher last week, bolstered by China’s outsized mortgage rate reduction and hopes for further stimulus. Nickel prices moved higher on U.S., UK and EU sanctions on Russian production. Aluminum prices, also subject to proposed U.S. sanctions, closed lower after the EU and UK did not include Aluminum as a sanctioned metal.

Grain prices were mixed with wheat prices rising and corn and soybean prices falling. Corn prices fell on the back of a strong Brazil harvest, favorable South American weather and rumors China was buying cheaper Ukraine corn. Soybean prices suffered from similar factors but with China opting for cheaper Brazil product. Wheat prices ended higher despite noticeably cheaper Russian and Ukraine product, perhaps benefiting from a weaker U.S. dollar and short covering early in the week.

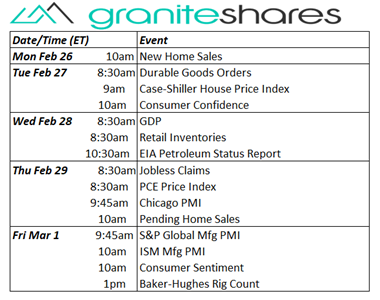

Coming Up This Week

Busier weak with durable goods orders, GDP and ISM and S&P Global PMIs. Attention, however, will be focused on Thursday’s PCE Price Index

Busier weak with durable goods orders, GDP and ISM and S&P Global PMIs. Attention, however, will be focused on Thursday’s PCE Price Index

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.