Commodities & Precious Metals Weekly Report: Mar 26

Posted:

Key points

Energy prices were were mixed last week with gasoline and natural gas prices higher, and WTI crude oil prices lower. Gasoline prices increased about 1.5% and natural gas prices rose just over 2%. WTI crude oil prices were 0.8% lower.

Energy prices were were mixed last week with gasoline and natural gas prices higher, and WTI crude oil prices lower. Gasoline prices increased about 1.5% and natural gas prices rose just over 2%. WTI crude oil prices were 0.8% lower.- Grain prices were all lower with wheat prices decreasing the most. Wheat prices fell between 2% and 3% while corn and soybean prices decreased 1%. Soybean oil prices dropped 2.5%.

- Base metal prices also were mixed. Aluminum and nickel prices increasesd with aluminum prices rising almost 1.5% and nickel prices gaining ½ percent. Copper prices fell just over 1% and zinc prices lost about ¼ percent.

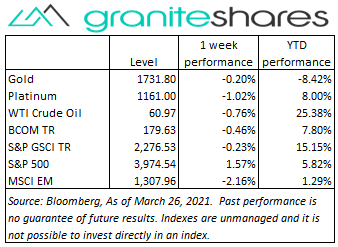

- Precious metal prices were all lower. Gold prices were down about ¼ percent, silver prices were lower by 4.5% and platinum prices dropped about 1%.

- The Bloomberg Commodity Index decreased 0.5% last week. Negative performance in the grains, precious metals and softs sectors was partially offset by slightly positive performance in the energy and livestock sectors.

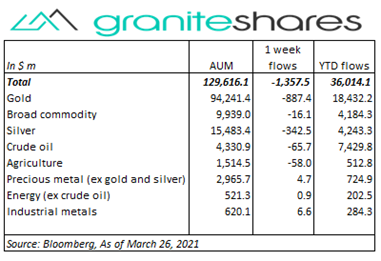

- Small ETP outflows last week with gold ETPs registering small inflows. Silver and crude oil ETPs saw outflows of $170 million and $100 million, respectively, while broad commodity ETPs had inflows of about $150 million. Gold ETPs saw inflows of $40 million.

- Just under $1.5 billion outflows from commodity ETPs with 2/3 of that coming from gold ETP outflows. Silver ETP outflows accounted for another ¼ with crude oil and agricultural ETP outflows comprising the remaining amount. There were no significant inflows last week.

Commentary

Another volatile week, this time with the S&P 500 and Dow Jones Indexes ending higher closing the week at record highs. The Nasdaq Composite Index, down almost 2% through Thursday, finished the week down 0.6%. Higher Monday on easing longer-term U.S. Treasury rates, U.S. stock markets dropped Tuesday and Wednesday following Treasury Secretary Yellen’s and Fed Chair Powell’s testimony before Congress, a much weaker-than-expected durable goods report and on global growth concerns spurred by renewed restrictions in Europe. Treasury Secretary Yellen’s comments suggesting the need for higher taxes and Fed Chair Powell’s caution regarding the pace of economic recovery may have helped move markets lower Tuesday and Wednesday. Lower-than-expected jobless claims, a revision higher to 4th quarter GDP and perhaps recovering oil prices moved stocks higher on Thursday and Friday, with major indexes rallying into the close on both days. 10-year U.S. Treasury rates, lower by 11bps through Wednesday, moved higher by almost 7bps the remainder of the week with most of that increase occurring Friday. For the week, the S&P 500 Index increased 1.6% to 3,974.54, the Dow Jones Industrial Average increased 1.4% to 33,072.88, the Nasdaq Composite Index decreased 0.6% to 13,138.74, the 10-year U.S. Treasury rate decreased 4bps to 1.69% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.9%.

Another volatile week, this time with the S&P 500 and Dow Jones Indexes ending higher closing the week at record highs. The Nasdaq Composite Index, down almost 2% through Thursday, finished the week down 0.6%. Higher Monday on easing longer-term U.S. Treasury rates, U.S. stock markets dropped Tuesday and Wednesday following Treasury Secretary Yellen’s and Fed Chair Powell’s testimony before Congress, a much weaker-than-expected durable goods report and on global growth concerns spurred by renewed restrictions in Europe. Treasury Secretary Yellen’s comments suggesting the need for higher taxes and Fed Chair Powell’s caution regarding the pace of economic recovery may have helped move markets lower Tuesday and Wednesday. Lower-than-expected jobless claims, a revision higher to 4th quarter GDP and perhaps recovering oil prices moved stocks higher on Thursday and Friday, with major indexes rallying into the close on both days. 10-year U.S. Treasury rates, lower by 11bps through Wednesday, moved higher by almost 7bps the remainder of the week with most of that increase occurring Friday. For the week, the S&P 500 Index increased 1.6% to 3,974.54, the Dow Jones Industrial Average increased 1.4% to 33,072.88, the Nasdaq Composite Index decreased 0.6% to 13,138.74, the 10-year U.S. Treasury rate decreased 4bps to 1.69% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.9%.

An extremely volatile week for oil prices, with WTI crude oil prices plummeting and surging 4% to 6% almost every day of the week. Slightly higher on Monday, WTI crude oil prices fell over 6% on Tuesday, reacting to new European restrictions and extended lockdowns due to increasing Covid-19 infections. Those losses were erased Wednesday with WTI crude oil prices jumping 6% mainly on news of a stuck ship blocking the Suez Canal. Increasing coronavirus-related concerns won the day Thursday with both Brent and WTI crude oil prices dropping 4%. News of a prolonged Suez Canal blockage took center stage Friday, pushing oil prices over 4% higher. For the week, WTI crude oil prices decreased 0.8%.

Despite decreasing longer-term U.S. Treasury rates and as-expected testimony by Fed Chair Jerome Powell, gold prices fell almost 1% through Tuesday, pushed lower by ongoing concerns of a less-accommodative Fed and a strengthening U.S. dollar. Extended lockdowns and new restrictions in Europe, growing concerns surrounding changes in U.S. tax rates and President Biden’s revealing of a $3 trillion recovery plan supported gold prices the remainder of the week, though with prices still ending slightly lower on the week. Silver and platinum prices moved lower but with silver prices decreasing much more sharply, falling almost 5% on the week.

Increased US, UK, EU – China tensions, coronavirus-related recovery concerns in Europe, growing concerns surrounding U.S. tax increases and a stronger U.S. dollar pushed base metal prices lower through Thursday, with copper prices, for example, down just over 3%. Sentiment reversed on Friday, however, buoyed by strong gains in U.S. stock markets and plans to greatly increase U.S. vaccinations, pushing most base metal prices 2% higher on the day.

Wheat prices were pressured lower by increased global supply estimates and favorable weather conditions in the U.S. Plain States. Soybean prices, up over 1% through Wednesday, fell Thursday and Friday on favorable weather expectations in South America, lower exports to China and expectations of increased planting in the U.S. Soybean oil prices up nearly 7% through Wednesday as a result of a global vegetable oil shortage and expectations of increased ethanol demand in the U.S, plummeted almost 10% over Thursday and Friday on no real news.

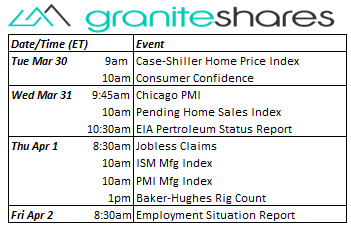

Coming up this week

Relatively light, holiday-shortened data week capped off with the Employment Situation Report on Friday when markets are closed.

Relatively light, holiday-shortened data week capped off with the Employment Situation Report on Friday when markets are closed.- Cash-Shiller Home Price Index and Consumer Confidence on Tuesday.

- Chicago PMI and Pending Home Sales Index on Wednesday.

- Jobless Claims and ISM and PMI Manufacturing Indexes on Thursday.

- Employment Situation Report on Friday.

- EIA petroleum status report on Wednesday and Baker-Hughes rig count on Thursday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.