Commodities & Precious Metals Weekly Report: Jun 18

Posted:

Key points

Energy prices were mixed with crude oil prices higher and derivatives and natural gas prices lower. WTI and Brent crude oil prices increased about 0.8% while gasoline and heating oil prices fell 1.25% and 0.5%, respectively. Natural gas prices decreased almost 2.5%.

Energy prices were mixed with crude oil prices higher and derivatives and natural gas prices lower. WTI and Brent crude oil prices increased about 0.8% while gasoline and heating oil prices fell 1.25% and 0.5%, respectively. Natural gas prices decreased almost 2.5%.- Grain prices were sharply lower. Chicago and Kansas wheat prices fell 3% and 5%, respectively. Corn prices dropped over 8% and soybean prices decreased almost 9%. Soybean oil prices dropped 12%.

- Base metal prices were sharply lower as well. Copper and zinc prices fell the most, decreasing 8.4% and 7.3%, respectively. Aluminum prices fell just over 3% and nickel prices decreased almost 6%.

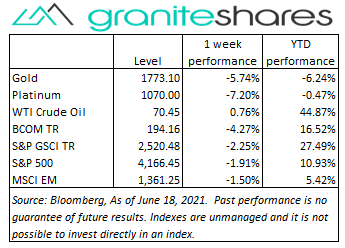

- Gold, platinum and silver prices were significantly lower, too. Gold prices lost nearly 6%, platinum prices fell over 7% and silver prices gave up nearly 8%.

- The Bloomberg Commodity Index decreased 4.3%, hurt mainly by poor performance in the grains, base metals and precious metals sectors. All sectors were lower on the week with the energy sector performing the best.

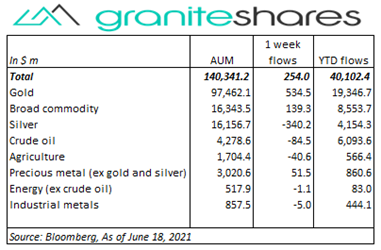

- Again small net inflows ($250mm) into commodity ETPs last week due to disparate flows. Gold ($534mm), broad commodity ($139mm) and precious metal (ex-gold and silver) ($52mm) ETP inflows were offset by silver (-$340mm), crude oil (-$85mm) and agriculture (-$40mm) ETP outflows.

Commentary

U.S. stock markets reacted negatively to the FOMC announcement Wednesday afternoon, with all three major indexes ending lower on the week. Monday, however, saw both the S&P 500 and Nasdaq Composite Indexes reach record highs with these levels gradually deteriorating into Wednesday’s announcement. The big news from the Fed was its shift forward in the timing of expected rate increases (on the heels of a record YoY PPI release Tuesday) as well as an increase in its inflation expectations. Interestingly, the Fed gave no guidance regarding its buyback program. Markets rebounded on Thursday but then sold off sharply Friday after St. Louis Fed President Jim Bullard opined that the first rate increase would occur in 2022. The Dow Jones Industrial Average fared the worst, falling each day of the week. The Treasury yield curve flattened, with 10-year U.S. Treasury rates declining slightly and 2-year U.S. Treasury rates rising 10bps, reflecting increased expectations of rate increases along with growing concerns of slowing economic growth. In addition, the U.S. dollar sharply strengthened. For the week, the S&P 500 decreased 1.9% to 4,166.45, the Nasdaq Composite Index fell 0.3% to 14,030.38, the Dow Jones industrial average dropped 3.5% to 33,290.08, the 10-year U.S. Treasury rate fell 1bps to 1.45% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 1.8% percent.

U.S. stock markets reacted negatively to the FOMC announcement Wednesday afternoon, with all three major indexes ending lower on the week. Monday, however, saw both the S&P 500 and Nasdaq Composite Indexes reach record highs with these levels gradually deteriorating into Wednesday’s announcement. The big news from the Fed was its shift forward in the timing of expected rate increases (on the heels of a record YoY PPI release Tuesday) as well as an increase in its inflation expectations. Interestingly, the Fed gave no guidance regarding its buyback program. Markets rebounded on Thursday but then sold off sharply Friday after St. Louis Fed President Jim Bullard opined that the first rate increase would occur in 2022. The Dow Jones Industrial Average fared the worst, falling each day of the week. The Treasury yield curve flattened, with 10-year U.S. Treasury rates declining slightly and 2-year U.S. Treasury rates rising 10bps, reflecting increased expectations of rate increases along with growing concerns of slowing economic growth. In addition, the U.S. dollar sharply strengthened. For the week, the S&P 500 decreased 1.9% to 4,166.45, the Nasdaq Composite Index fell 0.3% to 14,030.38, the Dow Jones industrial average dropped 3.5% to 33,290.08, the 10-year U.S. Treasury rate fell 1bps to 1.45% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 1.8% percent.

Oil prices hit 2-year highs early last week supported by expectations demand would outstrip supply in the coming months. OPEC+ production restraint, slow-to-react shale oil production, falling U.S. inventory levels and less sanguine Iran sanction outlooks combined to push prices higher. Wednesday’s FOMC announcement, indicating the Fed would tighten sooner than later, lowered demand expectations and strengthened the U.S. dollar, pushing oil prices significantly lower on Thursday. Some of Thursday’s losses were recouped Friday with both WTI and Brent crude oil finishing the week about ¾ percent higher.

Weaker ahead of the Wednesday’s FOMC announcement, gold prices plunged just under 5% Wednesday after the Fed indicated it may raise rates sooner than previously expected and raised its inflation expectations. The FOMC announcement pushed the U.S. dollar significantly higher last week contributing to gold’s price decline. Silver and platinum prices reacted with gold prices, but fell more sharply.

Copper prices suffered dual blows last week, reeling from China’s decision to release state reserves and from the Fed indicating it would move to increase rates sooner than later. China’s decision to release reserves acts to increase supply while the Fed’s apparent shift towards tightening increases expectations of slower economic growth while strengthening the U.S. dollar, both detriments to demand.

Another volatile week for grain prices. Corn and soybean prices, down just under 13% through Thursday, fell almost 7% Thursday and then rallied 5% Friday to close the week down about 8.5%. Wheat prices behaved similarly. Soybean oil prices also performed similarly but with siginficantly more volatility due to continued concerns regarding relaxation of biofuel blending requirements with gasoline. Changing weather expectations were the main driving force behind price movements, followed by a stronger U.S dollar and reports of hedge fund selling. Weather models flipped from hot and dry forecasts to wet and colder forecasts potentially providing relief to drought conditions in Plains and Midwest states, increasing harvest yield expectations and driving prices lower. Friday’s rally came as weather concerns resurfaced.

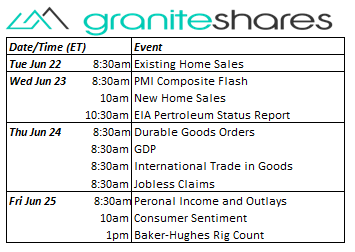

Coming up this week

Home sales data, PMI Composite Flash and GDP highlight a somewhat busy data-week.

Home sales data, PMI Composite Flash and GDP highlight a somewhat busy data-week.- Existing Home Sales on Tuesday.

- PMI Composite Flash and New Home Sales on Wednesday.

- Durable Goods Orders, GDP, International Trade in Goods and Jobless Claims on Thursday.

- Personal Income and Outlays and Consumer Sentiment on Friday.

- EIA petroleum status report on Wednesday and Baker-Hughes rig count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.