Commodities & Precious Metals Weekly Report: Jul 30

Posted:

Key points

Energy prices, except for natural gas prices, all rose last week with natural gas prices increasing the most. WTI and Brent crude oil prices rose just over 2.5%, gasoline prices increased 3 ¼ percent and heating oil prices gained just under 3%. Natural gas prices fell 3%

Energy prices, except for natural gas prices, all rose last week with natural gas prices increasing the most. WTI and Brent crude oil prices rose just over 2.5%, gasoline prices increased 3 ¼ percent and heating oil prices gained just under 3%. Natural gas prices fell 3% - Grain prices were mixed with wheat prices increasing and corn and soybean prices slightly falling. Chicago wheat prices increased almost 3% and Kansas wheat prices gained 4 ¼ percent. Corn and soybean prices fell 0.1% and 0.2%, respectively.

- Base metal prices were all higher. Aluminum prices increased 3.7%, copper prices increased 1.9%, zinc prices rose 2.5% and nickel prices gained 0.9%.

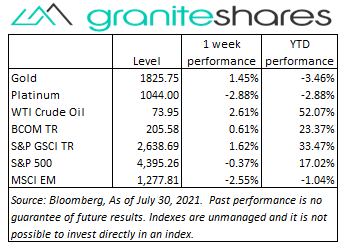

- Gold and silver prices rose and platinum prices fell. Gold prices increased about 1.5%, silver prices rose 1 ¼ percent and platinum prices fell 2.9%.

- The Bloomberg Commodity Index increased 0.6%, rising mainly as a result of the positive performances of the energy and base metals sector. The grains and precious metals sector also contributed to the Index’s return while the livestock and softs sector detracted from it.

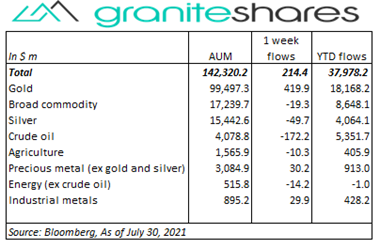

- Another week of net inflows ($214m) with gold ETPs ($420m) primarily responsible for the inflows and with crude oil ETPs (-$172m) mainly responsible for outflows.

Commentary

U.S. stock markets fell last week reacting to a myriad of inputs including GDP and PCE releases, the FOMC announcement and earnings reports. Markets struggled despite strong tech-company earnings reports Monday and Tuesday from Alphabet, Microsoft, Apple and Tesla with investors cautious before the FOMC announcement and the release of the first-estimate of Q2 GDP. Wednesday’s FOMC announcement, reporting no changes to monetary policy and slightly upgrading the assessment of the U.S. economy saying economic activity had strengthened and improved but not fully recovered, had little effect on stock prices. A worse-than-expected GDP release Thursday actually supported stock prices with all three major indexes ending the day higher. The first estimate of Q2 GDP growth came in at 6.5% economic growth versus expectations of 8.4%. The lower-than-expected number was attributed to production and transportation bottlenecks and to labor constraints. Friday’s higher-than-expected core PCE release and Amazon’s weaker-than-expected earnings report and slowing sales growth guidance pushed U.S. stock markets ½ to ¾ percent lower on the day. The U.S. dollar weakened significantly over the week, influenced by the combination of the Fed’s no-action mantra and growing inflation concerns. At week’s end, the S&P 500 Index decreased 0.4% to 4,395.26, the Nasdaq Composite Index fell 1.1% to 14,672.68, the Dow Jones Industrial Average decreased 0.4% to 34,935.47, the 10-year U.S. Treasury rate fell 5bps to 1.24% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 0.8% percent.

U.S. stock markets fell last week reacting to a myriad of inputs including GDP and PCE releases, the FOMC announcement and earnings reports. Markets struggled despite strong tech-company earnings reports Monday and Tuesday from Alphabet, Microsoft, Apple and Tesla with investors cautious before the FOMC announcement and the release of the first-estimate of Q2 GDP. Wednesday’s FOMC announcement, reporting no changes to monetary policy and slightly upgrading the assessment of the U.S. economy saying economic activity had strengthened and improved but not fully recovered, had little effect on stock prices. A worse-than-expected GDP release Thursday actually supported stock prices with all three major indexes ending the day higher. The first estimate of Q2 GDP growth came in at 6.5% economic growth versus expectations of 8.4%. The lower-than-expected number was attributed to production and transportation bottlenecks and to labor constraints. Friday’s higher-than-expected core PCE release and Amazon’s weaker-than-expected earnings report and slowing sales growth guidance pushed U.S. stock markets ½ to ¾ percent lower on the day. The U.S. dollar weakened significantly over the week, influenced by the combination of the Fed’s no-action mantra and growing inflation concerns. At week’s end, the S&P 500 Index decreased 0.4% to 4,395.26, the Nasdaq Composite Index fell 1.1% to 14,672.68, the Dow Jones Industrial Average decreased 0.4% to 34,935.47, the 10-year U.S. Treasury rate fell 5bps to 1.24% and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) weakened 0.8% percent.

Oil prices moved higher last week despite increasing Covid cases. Larger-than-expected declines in U.S. oil and distillate inventories combined with growing global demand helped drive prices higher for the week. A sharply weaker U.S. dollar, driven by the Fed’s continued no-change policy despite increasing inflation concerns, also helped support oil prices.

Gold prices moved higher last week powered by Wednesday’s FOMC announcement of unchanged accommodative monetary policy and of the Fed’s reluctance to increase rates in the foreseeable future. Slightly lower through Wednesday, gold prices rallied 1 ¾ percent Thursday powered by the Fed’s inaction and a weaker U.S. dollar. Friday saw gold prices give up some of Thursday’s gain precipitated by a stronger U.S. dollar.

Copper prices climbed nearly 5% Monday following an estimated $10 billion of damages due to flooding in China and, as a result, increased expectations of Chinese copper demand. Prices moved lower from Monday’s high and fell nearly 1% Friday after China auctioned a greater-than-expected amount of metal reserves. A weaker U.S. dollar and tight supply conditions supported base metal prices in general.

Wheat prices ended the weak higher bolstered by adverse weather concerns for the U.S. Midwest and by deteriorating crop conditions concerns. Soybean and corn prices, up nearly 2% through Thursday also on weather concerns, sold off sharply Friday on weaker-than-expected exports to end the weak slight lower.

Coffer prices, up nearly 10% Monday on frost-related crop damage in Brazil, moved lower the remainder of the week and nearly 9% lower Friday as damage concerns eased. Coffee prices ended the week 5% lower.

Coming up this week

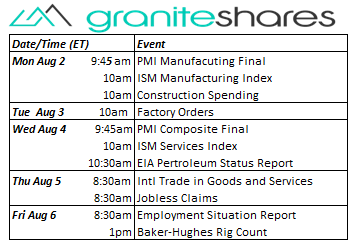

PMI and ISM manufacturing and services indexes occupying the first half of the week and jobless claims and the non-farm payroll report filling the latter half.

PMI and ISM manufacturing and services indexes occupying the first half of the week and jobless claims and the non-farm payroll report filling the latter half.- PMI and ISM Manufacturing Indexes and Construction Spending Monday.

- Factory Orders on Tuesday.

- PMI Composite and ISM Services Indexes on Wednesday.

- International Trade in Goods and Services and Jobless Claims on Thursday.

- Employment Situation Report on Friday.

- EIA Petroleum Status Report on Wednesday and Baker-Hughes Rig Count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.