Commodities & Precious Metals Weekly Report: Oct 16

Posted:

Key points

Energy prices were mixed with natural gas and WTI crude oil prices moving higher and gasoline and heating oil prices falling. Natural gas prices rose just under 2% and WTI crude oil prices moved slightly higher gaining just under ½ percent. Gasoline prices fell about 2%.

Energy prices were mixed with natural gas and WTI crude oil prices moving higher and gasoline and heating oil prices falling. Natural gas prices rose just under 2% and WTI crude oil prices moved slightly higher gaining just under ½ percent. Gasoline prices fell about 2%. - Wheat prices continued their move higher increasing between 4% and 5%. Corn prices also moved higher gaining just under 2% while soybean prices fell about 1.5%.

- Base metal all prices moved higher last week with the exception of copper prices. Nickel and aluminum prices increased the most with nickel prices increasing almost 3% and aluminum prices gaining 1.5%. Copper prices decreased about ½ percent.

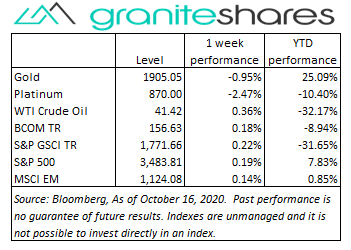

- Precious metal prices fell last week with gold prices decreasing about 1%. Silver and platinum prices fell about 2.5%.

- The Bloomberg Commodity Index edged slightly higher last week increasing 0.18%. The energy, grains and base metals sectors contributed to the increase while the precious metals and livestock sector detracted.

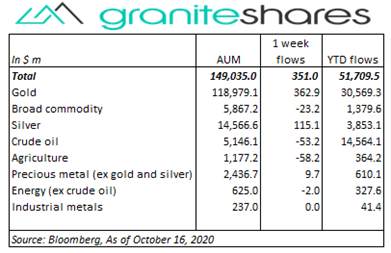

- Commodity ETP AUM increased $351 million primarily from gold and silver ETP inflows. Gold ETPs saw inflows of approximately $360 million and silver ETPs saw inflows of about $115 million. Crude oil and agricultural ETPs experienced outflows of about $55 million each.

Commentary

After surging Monday with tech stocks leading the way, U.S. stock markets sold off the remainder of the week mainly from reduced hope of a Congressional stimulus package and concerns about increasing Covid-19 cases. U.S. economic data released last week was mixed with a larger-than-expected jobless claims number and declining manufacturing production offset by much better-than-expected retail sales and higher consumer sentiment. At week’s end the S&P 500 Index increased 0.2% to 3,483.81, the Nasdaq Composite Index increased 0.8% to 11671.56, the 10-year U.S. Treasury rate fell 3bps to 74bps and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.7%.

After surging Monday with tech stocks leading the way, U.S. stock markets sold off the remainder of the week mainly from reduced hope of a Congressional stimulus package and concerns about increasing Covid-19 cases. U.S. economic data released last week was mixed with a larger-than-expected jobless claims number and declining manufacturing production offset by much better-than-expected retail sales and higher consumer sentiment. At week’s end the S&P 500 Index increased 0.2% to 3,483.81, the Nasdaq Composite Index increased 0.8% to 11671.56, the 10-year U.S. Treasury rate fell 3bps to 74bps and the U.S. dollar (as measured by the ICE U.S. Dollar index - DXY) strengthened 0.7%.

Down nearly 3% Monday on the back of increased production out of Norway, Libya and the Gulf, WTI crude oil prices jumped nearly 2% both Tuesday and Wednesday after much larger-than-expected China import numbers. Demand concerns prompted by reduced hopes of Congress passing a stimulus package and growing Covid-19 cases pushed WTI crude oil prices lower the remainder of the week

Gold prices moved lower last week with fading hopes for a U.S. stimulus package and a stronger U.S. dollar (especially against the Chinese yuan and the British pound) despite continued inflows into ETPs, increasing global Covid-19 infections and increasing concerns of slower economic growth. New coronavirus restrictions in Europe and Chinese central bank efforts to limit the strength of the yuan contributed to the U.S. dollar's strength.

Base metal prices moved higher on increased China demand expectations though reduced hopes of a U.S. stimulus package, increasing Covid-19 cases and a stronger U.S. dollar capped price gains. Copper prices, though down on the week, benefited from growing concern of wider copper mine strike in Chile.

Wheat prices moved sharply higher last week benefiting from increased concerns regarding production out of the U.S., South America and Russia as a result of continued dry weather and from increased global import demand. Corn prices increased with wheat prices and with strong Chinese demand. Soybean prices, down 3% on Monday on expectations of wet weather in Brazil, increased the remainder of the week as those expectations diminished and on strong demand.

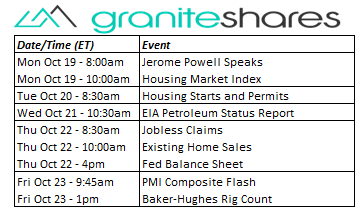

Coming up this week

Light data-week with focus on housing.

Light data-week with focus on housing.- Jerome Powell speaks and Housing Market Index on Monday.

- Housing Starts and Permits on Tuesday.

- Jobless Claims, Existing Home Sales and Fed Balance Sheet on Thursday.

- PMI Composite Flash on Friday.

- EIA petroleum report on Wednesday and Baker-Hughes rig count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.