Commodities & Precious Metals Weekly Report: Jun 7

Posted:Key points

- A mixed week for energy commodities. WTI and Brent crude oil prices reversed course increasing 0.9% and 1.7%, respectively, while gasoil, gasoline and heating oil prices fell 3.0%, 1.8% and 0.9%, respectively. Natural gas prices declined 4.7%.

- After weeks of gains, grain prices turned in a weak performance last week. Kansas wheat prices fell 5.1%, corn prices lost 2.6% and soybean prices decreased 2.5%. Chicago wheat prices finished slightly higher, increasing 0.3%.

- Base metal prices were all lower last week. Aluminum and zinc prices decreased 2.0%, and copper and nickel prices decreased 0.5% and 3.5%, respectively.

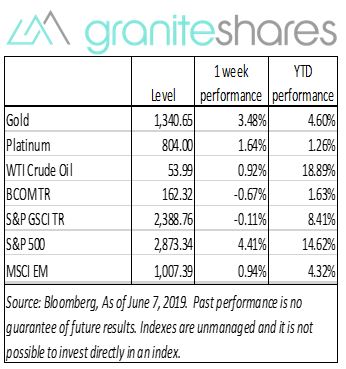

- Gold prices moved higher again last week. Platinum and silver prices also increased. Gold prices rose 3.5%, platinum prices gained 1.6% and silver prices rose 3.2%.

- Lean hog and cotton prices closed limit down on Friday, ending the week down 3.0% and 3.5%, respectively. Coffee prices fell 3.5%.

- The S&P GSCI outperformed the Bloomberg Commodity Index last week with the S&P GSCI decreasing 0.11% and the Bloomberg Commodity Index declining 0.67%. The S&P GSCI’s larger exposure to WTI and Brent crude oil but lower exposure to natural gas was primarily responsible for its outperformance,

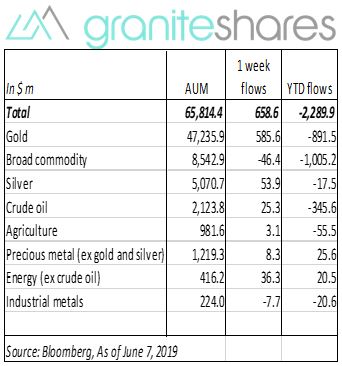

- Total assets in commodity ETPs increased $658.6m last week. Gold ($585.6m), silver ($53.9m), energy (ex-crude oil) ($36.3m) and crude oil ($25.3m) ETP inflows were offset primarily by broad commodity (-$46.4m).

Commentary

Amid growing concerns of a slowdown in U.S and global growth resulting from continued trade frictions between the U.S. and China and more recently with the U.S. and Mexico, U.S. Federal Reserve Bank officials indicated the U.S. Federal Reserve Bank may need to lower rates in the near future. After Friday’s much-weaker-than-expected employment report, market expectations of a rate reduction increased to over 80% in the July FOMC meeting and reached near 100% for the September meeting. Bouyed by increasing expectations of a rate cut, the S&P 500 Index finished the week up 4.4%, U.S. dollar weakened 1.2% and the 10-year U.S. Treasury rate fell 4.5bps to 2.08%

Down 3.4% through Wednesday mainly as a result of increased trade frictions between the U.S. and Mexico, a much-greater-than-expected increase in U.S. oil inventories and record U.S. oil production, WTI crude oil prices rallied 4.5% Thursday and Friday after OPEC indicated production cutbacks would continue beyond the end of this month and on Trump administration statements suggesting significant progress had been achieved in negotiations with Mexico possibly preventing the implementation of tariffs on imports from Mexico.

Despite a much weaker U.S. dollar, base metal prices fell on increased concerns of weaker Chinese, U.S. and global economic growth.

Gold prices moved higher buoyed by a weaker U.S. dollar, increased expectations of a U.S. Federal Reserve Bank rate decrease, DOJ and U.S. anti-trust investigations on Google and Amazon and increased geopolitical tensions particularly between the U.S and China and the U.S. and Mexico. Silver and platinum prices moved higher with gold prices.

Volatile week for grain prices. Kansas wheat prices rallied 3% Monday on forecasts of continued wet and stormy weather only to fall over 8% over the next two days after better-than-expected USDA crop condition reports and improved Black Sea weather forecasts Wheat prices rose sharply on Thursday with adverse weather forecasts reducing forecasted yields of Russian and Australian grains only to reverse most of those gains on Friday as those concerns diminished. Soybean prices declined on lower-than-expected China imports and corn prices fell on expectations of improved conditions for plantings.

Coffee prices fell on as a result of a stronger Brazilian real/weaker U.S. dollar and cotton prices continue to suffer from U.S-China trade frictions.

Coming up this week

- Inflation numbers on Tuesday and Wednesday. PPI on Tuesday and CPI on Wednesday.

- Jobless claims on Thursday.

- Retail sales, industrial production and consumer sentiment on Friday.

- EIA petroleum report on Wednesday and Baker-Hughes rig count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.