Commodities & Precious Metals Weekly Report: Jul 24

Posted:Key points

Energy prices all moved higher last week with gasoline and natural gas prices increasing the most. WTI and Brent crude oil prices increased 1.3% and 1.5%, respectively. Gasoil and heating oil prices increased 1.9% and 2.6%, respectively and gasoline and natural gas prices rose 5.8% and 4,1%, respectively.

Energy prices all moved higher last week with gasoline and natural gas prices increasing the most. WTI and Brent crude oil prices increased 1.3% and 1.5%, respectively. Gasoil and heating oil prices increased 1.9% and 2.6%, respectively and gasoline and natural gas prices rose 5.8% and 4,1%, respectively.- Grain prices were mixed last week again. Chicago and Kansas wheat prices increased 0.9% and 0.2%, respectively and soybean prices increased 0.5%. Corn prices fell 2.0%.

- Base metal prices, except for copper prices, were all higher (the opposite of the previous week’s performance). Aluminum, zinc and nickel prices rose 2.3%, 1.7% and 3.3%, respectively. Copper prices fell 0.4%.

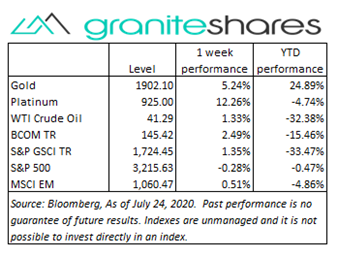

- Gold, silver and platinum prices all rose last week with silver and platinum prices surging. Gold prices gained 5.2% while silver and platinum prices jumped 15.6% and 12.3%, respectively.

- The Bloomberg Commodity Index increased 2.49% last week benefiting mainly from strong performances in the energy and precious metals sectors. The grains and livestock sectors were the only negative performing sectors with only slightly negative returns over the week.

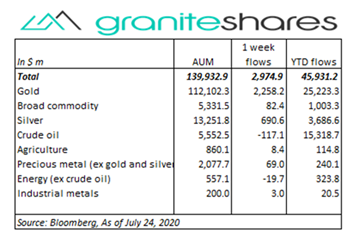

- Total assets in commodity ETPs greatly increased last week, with new inflows of $2,974.9m. As has been the case in previous weeks, gold ETP inflows were primarily responsible for the increase though inflows into silver ETPs also were significant. ETP inflows included gold ($2,258.2m), silver ($690.6m), broad commodity ($82.4m) and precious metal (ex-gold and silver) ($69m). Crude oil (-$117.1m) ETP outflows continued again last week with no other significant ETP outflows.

Commentary

Riding on the previous week’s momentum, U.S. stock markets moved higher on Monday with the Nasdaq Composite Index reaching another record high. Increased investor optimism spurred by the EU’s passage of an $860 billion coronavirus recovery fund, increased hopes of a phase 4 U.S. coronavirus stimulus package and positive developments regarding a Covid-19 vaccine helped move the S&P 500 Index higher through Wednesday. Despite a strong Microsoft earnings report after the close on Wednesday, both the S&P 500 and the Nasdaq Composite Index moved lower on Thursday with the Nasdaq Composite Index falling over 2%. A larger-than-hoped-for jobless claims number, new U.S-China frictions resulting in the closing of the China consulate in Houston, rising Covid-19 cases and the rotation out of tech into cyclical stocks all contributed to Thursday’s as well as Friday’s U.S. stock market declines. The U.S. dollar (as measured by the U.S. Dollar Index – DXY) weakened significantly over the week, pressured lower by increased concerns over the growing number of U.S. Covid-19 cases, uncertainty regarding a phase 4 coronavirus stimulus package and expectations EU GDP growth will significantly outpace U.S. GDP growth over the next year. At week’s end the S&P 500 Index decreased 0.3% to 3,215.63, the Nasdaq Composite Index fell 1.3% to 10,363.18, the 10-year U.S. interest rate fell 4 bps to 59bps and the U.S. dollar (as measured by the U.S. Dollar index - DXY) weakened 1.7%.

Riding on the previous week’s momentum, U.S. stock markets moved higher on Monday with the Nasdaq Composite Index reaching another record high. Increased investor optimism spurred by the EU’s passage of an $860 billion coronavirus recovery fund, increased hopes of a phase 4 U.S. coronavirus stimulus package and positive developments regarding a Covid-19 vaccine helped move the S&P 500 Index higher through Wednesday. Despite a strong Microsoft earnings report after the close on Wednesday, both the S&P 500 and the Nasdaq Composite Index moved lower on Thursday with the Nasdaq Composite Index falling over 2%. A larger-than-hoped-for jobless claims number, new U.S-China frictions resulting in the closing of the China consulate in Houston, rising Covid-19 cases and the rotation out of tech into cyclical stocks all contributed to Thursday’s as well as Friday’s U.S. stock market declines. The U.S. dollar (as measured by the U.S. Dollar Index – DXY) weakened significantly over the week, pressured lower by increased concerns over the growing number of U.S. Covid-19 cases, uncertainty regarding a phase 4 coronavirus stimulus package and expectations EU GDP growth will significantly outpace U.S. GDP growth over the next year. At week’s end the S&P 500 Index decreased 0.3% to 3,215.63, the Nasdaq Composite Index fell 1.3% to 10,363.18, the 10-year U.S. interest rate fell 4 bps to 59bps and the U.S. dollar (as measured by the U.S. Dollar index - DXY) weakened 1.7%.

WTI crude oil prices mostly mirrored U.S. stock market performance last week with prices rising through Wednesday and then moving lower through Friday. Up nearly 3% through Wednesday (reaching a 4-month high) mainly on positive Covid-19 vaccine developments, WTI oil prices slid 2% on Thursday after a disappointing jobless claims report and increasing tensions between the U.S and China. Natural gas and, for the most part, gasoline prices moved higher throughout the week boosted by production concerns with the development of tropical storm Hanna in the Gulf of Mexico.

A significantly weaker U.S. dollar and the EU’s agreement on an $860 coronavirus recovery fund helped move most base metal prices higher last week. Perhaps reacting to increased U.S.-China frictions, all base metal prices moved lower on Friday. Copper prices, for example, up 1.2% through Thursday, fell 1.6% on Friday.

Up over 5% on the week, gold prices closed at of $1902.1 per ounce on Friday, their all-time-closing-level high. Silver prices, though closing off their Thursday’s high, surged over 15%, reaching their highest levels since 2014. Platinum prices, surging over 12%, climbed to their highest levels since late February this year. Precious metal prices already supported by unprecedented monetary and fiscal stimulus, benefited from increased tensions between the U.S and China, increased concerns about U.S. economic growth in light of growing Covid-19 cases and a significantly weaker U.S. dollar (as measured by the U.S. Dollar Index – DXY).

Soybean prices moved higher with strong exports (including China exports). Corn prices, too, benefited from strong export numbers but suffered from expectations of record crop harvests helped out by forecasts of favorable weather conditions. Wheat prices moved higher with stronger Russian export prices. All grain prices benefited from a weaker U.S. dollar.

Coming up this week

Busy data-week including 2-day FOMC meeting beginning Tuesday and the first estimate of 2nd quarter GDP on Thursday.

Busy data-week including 2-day FOMC meeting beginning Tuesday and the first estimate of 2nd quarter GDP on Thursday.- Durable goods orders on Monday.

- FOMC meeting begins and consumer confidence on Tuesday.

- International trade in goods, pending home sales index and FOMC announcement and press conference on Wednesday.

- First estimate of 2nd quarter GDP, jobless claims and Fed balance sheet on Thursday.

- Personal income and outlays, employment cost index, Chicago PMI and consumer sentiment on Friday.

- EIA petroleum report on Wednesday and Baker-Hughes rig count on Friday.

Who is Jeff Klearman in our research team? Jeff has over 20 years experience working as a trader, structurer, marketer and researcher. Most recently, Jeff was the Chief Investment Officer for Rich Investment Services, a company which created, listed and managed ETFs. Prior to Rich Investment Services, Jeff headed the New York Commodities Structuring desk at Deutsche Bank AG. From 2004 to 2007, he headed the marketing and structuring effort for rates based structured products at BNP Paribas in New York. He worked at AIG Financial Products from 1994 to 2004 trading rates-based volatility products as well as marketing and structuring. Jeff received his MBA in Finance from NYU Stern School of Business and his Bachelors of Science in Chemical Engineering from Purdue University.